Port of London Economic Impact Study

The full study is available in PDF format The full study is available in PDF format |

Summary report | Spring 2020

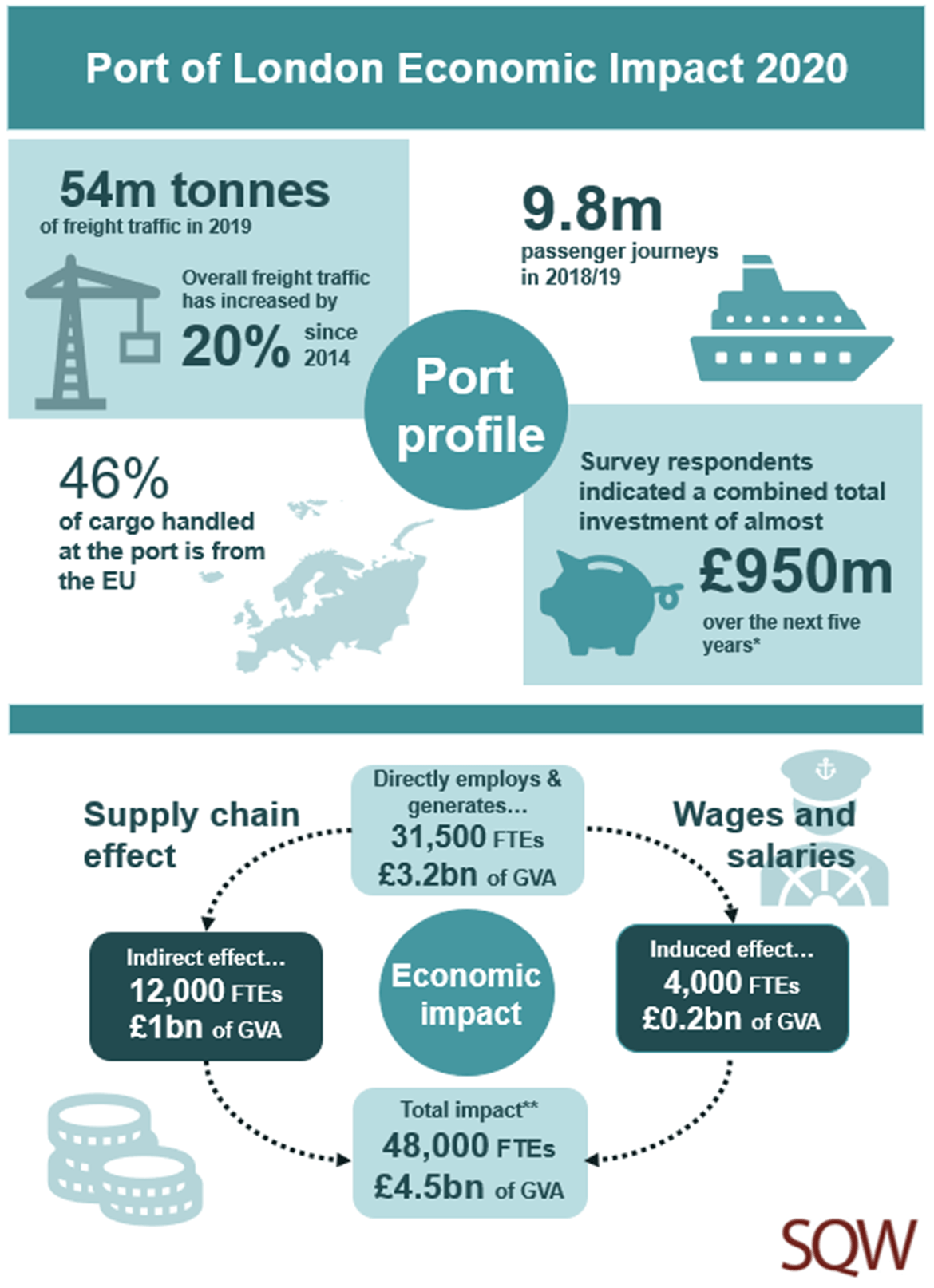

The Port of London Authority appointed SQW in February 2020 to estimate the direct and indirect economic impact of port activities across defined geographic areas and identify trends. This provides an update on progress in the delivery of the Thames Vision 2035, our collaborative plan for sustainable growth in use of the Thames, which was launched in 2015 alongside a similar study. The study estimates a total direct and indirect impact of around 48,000 FTEs and a GVA contribution of £4.5bn, offering a snapshot of activity just prior to the onset and economic effects of the Covid-19 pandemic in the UK. It provides a focus for our efforts with stakeholders, to be reflected in a refreshed Thames Vision, to sustain this activity as part of the economic recovery and move beyond it to a sustainable future.

The Port of London is one of the largest ports in the UK, handling 54 million tonnes of freight in 2019 and growing 20% over the past five years compared to an overall 3% fall in the freight tonnage handled by all UK major ports. Reflecting its status as a major port, London deals with freight traffic from around the world, with EU freight traffic particularly prominent. In addition, there are also significant volumes of passengers who use the Thames, with around 10 million journeys made per year.

Total impact summary

| Geographic Area |

Employment (FTE) |

GVA (£m) |

|---|---|---|

|

London |

19,141 |

1,788 |

|

Essex |

12,607 |

1,211 |

|

Kent |

5,110 |

537 |

|

Rest UK |

10,466 |

848 |

|

Overseas |

417 |

71 |

|

Total |

47,741 |

4,455 |

Source: SQW